NPD DisplaySearch: LCD TV Growth Improving, As Plasma and CRT TV Disappear

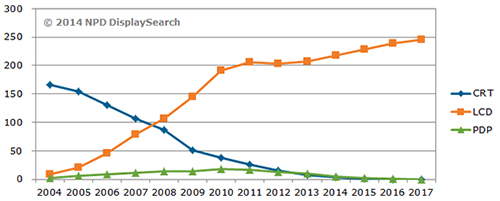

Since reaching a peak in 2011, the global TV market has seen continuous declines, falling by 6 percent in 2012 and by 3 percent in 2013. LCD TV shipment growth fell into single digits in 2011, experienced its first decline in 2012, and grew by only 2 percent in 2013, which was not enough to make up for falling shipments of plasma and CRT TVs. With LCD surpassing 90 percent of global TV shipments, it is the dominant driver of industry growth.

According to the latest TV market forecast published in the NPD DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report, worldwide TV shipments are projected to grow less than 1 percent in 2014, but LCD TV shipments will rise almost 5 percent. Of course, the growth of LCD comes at the expense of plasma and CRT TV shipments, which are forecast to fall 48 percent and 50 percent, respectively, in 2014. Both technologies will all but disappear by the end of 2015, as manufacturers cut production of both technologies in order to focus on LCD, which has become more cost competitive. OLED is expected to grow as an alternative flat panel display technology for TVs but is expected to account for less than 1 percent of shipments through 2017.

“TV shipments worldwide have struggled for the past few years, as several unusual events have disrupted normal buying patterns,” according to Paul Gagnon, director for global TV research at NPD DisplaySearch. “Governments instituted subsidy programs to prop up local economies in the post-recession years from 2009 through 2013, and digital-to-analog broadcast transitions for many developed and emerging countries accelerated demand for TVs further at the expense of future demand.”

Figure 1: Forecast for LCD TV, Plasma TV and CRT TV Unit Shipments

Source: NPD DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report

Developed Region Growth Stabilizes, While Emerging Region Growth Remains Soft

The collective emerging regions of the world have long dominated global TV demand. However, at the end of the last decade, TV demand growth surged in developed regions, which included Japan, Western Europe and North America. Much of this increased growth rate was due to analog broadcast shut-off events, as well as rapid cost reductions on flat panel TVs. Japan and other governments also implemented spending programs to boost local demand for energy-efficient TVs and other products. Since then, shipments have declined significantly, as future demand was satisfied during the boom years, though demand has stabilized at around 75 million units annually.

Meanwhile, emerging region growth accelerated from 2009 through 2012, as demand from China skyrocketed, due to several local subsidy programs. With China’s subsidy program now ended and CRT demand falling more quickly than LCD can grow in Asia Pacific and other regions, growth factors have turned distinctly weaker for emerging regions. The World Cup in 2014 and Summer Olympics in 2016, both of which occur in Brazil, will likely have a stimulus effect on many emerging countries. Finally, the end of CRT TV availability will transition purchasing behavior to flat panel TVs.

Figure 2: TV Shipments by Regional Category

Source: NPD DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report

The DisplaySearch Q1’14 Quarterly Advanced Global TV Shipment and Forecast Report, available now, includes panel and TV shipments by region and by size for nearly 60 brands. It also includes rolling 16-quarter forecasts, TV cost/price forecasts, and design wins. For more information about the report, please contact Charles Camaroto at 888-436-7673 or 516-625-2452, email contact@displaysearch.com.

More Stories Like This

Rohde & Schwarz to Demonstrate Energy-Efficient Technology Innovation at IBC2024

Rohde & Schwarz is bringing the latest technologies in television and radio transmission to IBC2024. The company will show how innovative designs are delivering unprecedented efficiency for transmitters and enabling broadcast network operators to address new business opportunities and make greater strides in sustainability. The R&S®TH1 liquid-cooled high-power transmitter is the solution of choice for […]

The Daily Raff: ISE 2024 Day 2 Thoughts

Hello, everyone! Welcome to ISE 2024 and therefore, your ISE 2024 Day Two Daily Raff article. I’ll be honest. Today, I mostly ran around the show floor (quite frequently between Halls 3 and 5) and GOOD LORD. Hall 3 was so packed, you couldn’t move. It was almost like a general admission concert. And maybe […]

LG Display to Supply High-End TV Panels to Samsung Electronics — What Does This Mean?

In a wild twist of fate, Reuters is reporting that, “South Korea’s LG Display Co Ltd (034220.KS) will start supplying high-end TV panels to Samsung Electronic Co Ltd (005930.KS) from as early as this quarter, three sources said, in a deal that would help the loss-making flat-screen maker turn profitable.” Well, what do we have […]