2010 – The Year of Choice… On How To Engage with Digital Signage

The “train” that is Digital Signage left the station in the post 9/11 economy when advertisers and marketers sought more productive ways of communicating. Since then it has been picking up speed at a double digit compound annual rate of growth and acceleration, and now has a full head of steam and is thundering down the tracks in just about every market and application area.

Digital signage continues to be installed at points of purchase, transit, waiting and gathering, at and near where people shop, work and study to inform, influence and increase safety.

Arbitron has reported that Out-of-Home video as a medium reaches 67 percent of Americans 18 years and older each month, and delivers a fairly representative cross-section of consumers. 76 percent of those seeing digital signage noticed displays in multiple venues.

A “critical mass” of displays has been deployed, which allows advertisers to reach targeted audiences based on demographic profile, Designated Market Area (DMA), geography and even the activity in which they are involved (shopping, transit, café, workout, attending a game, etc.). More than 180 ad-based networks exist with 47 of these (as Out-of-Home Video Advertising Bureau – OVAB members), accounting for almost 400,000 displays. DisplaySearch reflects that almost 1 million displays have been deployed in North America for dynamic media presentation to shoppers, patrons, staff and students. A Compound Annual Growth Rate (CAGR) in display deployment of 23 percent+ is forecast. This growing critical mass substantiates the value of the medium for marketers and other communicators.

20 percent of the 1200 firms that responded to the fall 2009 industry survey conducted by the Digital Signage Association indicate they will spend between $200K and $1M per year on DS/DOOH. This represents 240 firms of the survey respondents themselves expecting to spend a total of $48 to $240 million. Forecasts by industry analysts place industry projections in excess of $1.2B annually.

So the question is not whether or not an end user or suppler organization will engage with digital signage during 2010, but “how.” End users, suppliers and integrators all have the choice to be part of digital signage or not, with consequences to those that do not, and benefits for those organizations that do.

End users such as retailers, service providers and others will lose revenues and patrons to competitors that use the medium, or will enjoy the benefits of more effective communications spending, meeting the information needs of target audiences. We are increasingly a “visual” society and the effectiveness of digital signage as a communications device is being proven across a wide spectrum of projects.

AV and IT integrators are ideally suited to providing the technology integration needed. Some have lost market positioning by not offering digital signage earlier, while others have seized on new clients, revenues and margins, while other parts of their business have declined. Some are generating new, ongoing revenues from services such as network planning and design, network operations and content production. End users are going to buy from someone, and the ability to respond to needs is the basis of ongoing supply relationship.

The field of the suppliers of technologies that comprise the technology “ecosystem” continues to grow. While some bring more cost/effective elements for media authoring, management, connectivity and presentation, many are enhancing their offering by bundling technology elements.

Once the choice of whether to engage is made, the important question of “how” needs to be addressed.

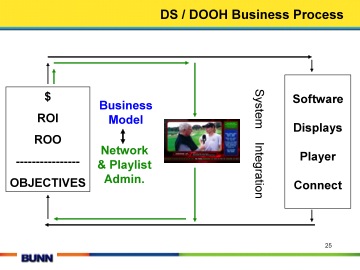

The following chart illustrates the framework for digital signage planning, supply and operations. It provides the context of the choices that end users and suppliers must make as they decide HOW they will engage with DS.

No single organization can supply all elements of a Digital Signage network and there are a wide range of more or less encompassing approaches used in both the sourcing and supply of the required elements. This presents opportunities while also making decisions about sourcing and supply both important and complex.

|

Digital signage starts in the same way as the typical audio/visual project; however, they are typically much more complex in the definition of intended use, outcomes, Return on Investment (ROI) and Return on Objectives (ROO). A challenge of this phase is that the lack of understanding of what the digital signage technology can do, often constrains the process.

So consideration for the enabling technology in terms of functionality/benefits/costs relative to ROI and ROO is needed. The iteration and refinement of communications goals and the technology will result in a balance of outcome versus investment.

During this planning and assessment, the approach to technology sourcing/supply will be determined.

This feeds into the business model of “who supplies what” and “how.”

And in this process, some areas of ongoing operation emerge as key sourcing/supply issues. These include network operations, help desk, playlist administration, and content creation and sourcing in particular.

Throughout the process, end users as well the integrator and suppliers must each decide on the nature and degree of their involvement in each phase of the system deployment life cycle and the sourcing of required technologies and services.

New digital signage projects will be advancing in 2010 across the economy. And, as the communications objectives become broader in scope and the technology infrastructure of existing networks is refreshed, new sourcing requirements and supply opportunities exist.

So, 2010 is a year of choices.

Correct decisions by end users will result in successful projects with ROI/ROO from the sourcing and use of digital signage.

Correct decisions by integrators and suppliers will result in new revenues and profits, the retention of existing customers and expansion through new ones.

Lyle Bunn is a highly regarded independent consultant and educator in North America’s Digital Signage Industry. He is a member of the Academy Faculty of InfoComm, has published over 80 articles and regularly presents at industry events. He is author and principal presenter of the SPEED Digital Signage Training Program which was used by over 1100 people during 2009 to plan their project and supply approaches. Go to http://www.LyleBunn.com or email him at Lyle@LyleBunn.com

More Stories Like This

Digital Signage Guru Lyle Bunn Dies After Battle With Cancer

The first digital signage industry advocate I ever met was Lyle Bunn, recent founder of The Center For Digital Experience. It must have been some 20 years ago and I was writing for Sound and Communications magazine at the time. They asked us to do a new video show they were producing at the time.I […]

Learn More About Digital Signage This Wednesday in a Webinar With Lyle Bunn

THIS IS A PROMOTED POST Almo Pro AV will host industry expert Lyle Bunn, Centre for Digital Experience Chair as guest speaker for its November LG Spotlight Series webinar. Start planning your strategy for 2018 and join Almo as Bunn looks ahead to discuss upcoming trends in the digital signage space. The contribution of distributors, […]

The Outlook for Digital Signage in 2017 Is More, More, More

Yogi Berra wasn’t referencing digital signage when he said, “It’s very tough to make predictions, especially about the future.” Digital signage and place-based media can apply present status, and, with a wide enough view of the lens and clarity into the depth, know what is coming in 2017. The proposition is simple. More digital signage […]