DisplaySearch Sees Recovery in the Display Industry

By Norbert Hildebrand

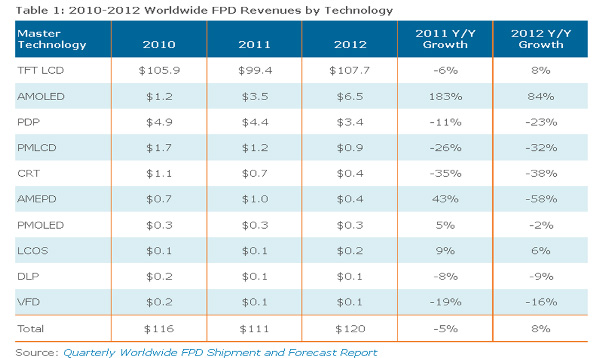

DisplaySearch just released its new Quarterly Worldwide FPD Shipment and Forecast Report. They forecast a recovery of the display industry for 2012. According to the data, the total sales volume of the industry will grow to $120 billion in 2012 from $111 billion in 2011. The new number even exceeds the result form 2010 and shows a 8 percent growth YoY.

DisplaySearch also breaks the sales numbers down by display technology, which shows that TFT LCD is undisputed king of the display world at the moment. In the number two spot they see AMOLED with sales of $6.5 billion ahead of PDP with $3.4 billion. This is the first year where AMOLED is ahead of PDP by sales $. The impressive part is the 84 percent YoY growth of AMOLED versus a 23 percent decline for PDP. Of course the weak TV market and lower priced large size LCD TVs are marking a significant challenge for the PDP technology. Even with lower priced 720p panels, PDP has lost more market share against TFT LCD and it seems unlikely that they will be able to recover and re-take significant market share.

TFT LCD on the other hand showed some growth, mainly driven by higher priced high-resolution panels for mobile devices. Indeed, all display technologies tracked by DisplaySearch showed a decline besides TFT LCD, AMOLED and LCOS.

It seems that the display industry is more and more focusing on a few display technologies to cover all applications. Only the top three display technologies (TFT LCD, AMOLED and PDP) hold more than a 1 percent market share. According to the numbers from DisplaySearch the display industry is currently following more of 90/10 market rule (90 percent of the technologies account for only 10 percent of the market) rather than a the typical 80/20. With continued growth of the AMOLED technology this may change back to the 80/20 rule rather quickly.

The key driver for more AMOLED usage is of course the mobile sector where AMOLED should have some intrinsic advantages. With the weak TV market worldwide the importance of mobile display devices will continue to grow and with it the AMOLED technology. If AMOLED can achieve satisfactory yields for large panels in the very near future, the next big TV boom might indeed be driven by AMOLED displays.

According to their numbers, electrophoretic displays (AMEPD) shrunk by as much as 58 percent YoY after they managed a 43 percent growth the year before. DisplaySearch blames the success of Tablets as the main reason for the decline in electronic book reader sales (EBR) as the main driver for AMEPD sales. As E-Ink is the main supplier in the market today, it seems that we will have to wait and see how the main selling season (last quarter in a CY) affects their overall sales. We know that the gross margin at E-Ink has shrunk substantially from 2011 to 2012. This could be a result from lower sales as well as declining display prices. Since the new Kindle has a higher resolution, the backplane cost has definitely not decreased, and the effect of the new Kindle as well as the Nook will only be seen in the coming quarter. I would not be surprised if the decline of the AMEPD will be actually lower than expected.

More Stories Like This

Can Ultra-Slim LCD TV Compete With OLED TV?

By Jimmy Kim DisplaySearch Ultra-slim has become a main feature for mobile PCs, and TVs are also trying to capitalize on this trend. Recently, Sony officially launched its Bravia X900C and X910C series LCD TVs described as having “ultra-thin floating styles” with only 4.9 mm thickness. With OLED TV being promoted with under 5.0 mm […]

The 43″-Panel Market Poised to Grow Rapidly

By Ricky Park DisplaySearch There are signs of a big change in 2015 in the 43” (42.5”) panel market. LG Display started releasing 43” panels in H2’14, and with the support of LG Electronics, as well as a strong competitor AU Optronics (AUO) joining in the supply market, shipments of 43” panels in March 2015 […]

What If an Integrated Service Provider Offers Free LCD TVs?

By David Hsieh DisplaySearch Recently, there has been discussion in the Chinese LCD TV supply chain about offering free LCD TVs as a promotional tool. The conversations are a result of Alibaba, the big e-commerce provider in China, possibly planning to introduce a TV, the Ali-TV, as a shopping platform for its users. The biggest […]