|

Volume 13, Issue 15 — August 11, 2016

|

Editorial

Editorial

Editorial

Editorial

Editorial

|

|

Industry News

Cables, Furniture, Mounts, Racks, Screens and Accessories

Control & Signal Processing

Audio

|

|

|

Integration Is What You Do — Not What Apple, Google and Amazon Do

By Gary Kayye

rAVe Founder

CEDIA CEO Vin Bruno recently told a group of residential integrators that his organization wants to help the AV integration community transition away from using the term “integrator” and move towards using the term “technologist.”

While I applaud CEDIA for proactively moving towards helping the integration community as a whole — something they clearly haven’t done in a half-dozen or so years — this isn’t the way to do it.

Yes, it’s admirable that Vin is attempting to help hone-in on what helps an end-user find an integrator for their smart homes or home entertainment systems, but this isn’t the time to focus on that. CEDIA should be focusing on how to help the INTEGRATOR community fend-off the deluge of stolen business thanks to the likes of Apple, Google, Best Buy, Amazon, etc. It’s only going to get worse as the Echo and Alexa (as well as Siri, apparently, with Apple’s new HOME app) take away some of the magic from companies like URC, Control4, Xantech, Savant, etc.

There isn’t a single integration firm I’ve spoken to in the past year that isn’t feeling the effects of one or more of those companies. And, the manufacturers are too — some of CEDIA’s largest exhibitors have told me that they have slowed R&D spending while waiting to see what Apple and Google’s strategies are.

The very high-end of the market is thriving, the low-end is gone (and good riddance), but the middle of the market is isn’t sure what to do. Changing the branding or, in this case, the most recognizable term that actually describes what a HomeAV integration firm does, isn’t the solution to the slowed growth.

CEDIA should focus on building bridges. Why isn’t Apple at CEDIA? Why isn’t Google there? Do we pretend they don’t exist and don’t affect us? Do we hope that they don’t?

Recent trends that are liable to be devastating to HomeAV include:

- 30-somethings (and younger) don’t watch TV on giant screens — they do it on tablets, phones and regular TVs that have content streamed via $99 set-top boxes on 9-watt speakers. And, even scarier (or you should at least note), Pokémon GO is teaching adults that small screens aren’t just for second screening TV — that primary content is OK being viewed there — so this “trend” may not be relegated to 30-somethings for long.

- Cable TV use, satellite TV use and music listening are all in decline. Streaming is up but traditional, system-based technologies, are heading down — and this isn’t a trend.

- Voice-based and gesture-based control are on the emerging horizon and they aren’t being driven by the likes of the big control system companies — they’re being pioneered and closely controlled (and managed) by Facebook, Apple, Google and Amazon (and now Microsoft). This is all under the mantra of simplification.

- Only one TV company in the world was profitable last year.

- Two the the top-five whole house audio companies saw greater than 20 percent declines for the second year in a row.

- The average price of a 2-meter HDMI cable is $11.36

- Crestron pulled out of CEDIA Expo. This matters. Don’t kid yourself to think that other manufacturers aren’t considering it. In the past two weeks, two of CEDIA’s 20 largest exhibitors told me this could be their last show on the floor (although, they wanted to make it clear to me they still support the organization). I will write more on this later this fall.

Do NOT assume (by reading this) that I am down on the HomeAV market as I am not. In fact, I see 4K as a guarantee that 2017 will be a hell of a lot better year for the HomeAV community than 2016. 4K is complicated, doesn’t work with nearly ANY of the infrastructure installed today and takes a very-detailed integrator (not a technologist) to specify and build a system properly. So, you’ll make a fortune selling and INTEGRATING (not technologisting) 4K systems.

However, I don’t believe that marketing-speak will fix a much bigger issue. Let’s not pretend the 800-pound gorilla isn’t in the room. Calling him a monkey instead of a gorilla won’t make him less likely to kill you. Leave a Comment

Share Article

Back to Top |

Click above to learn more

|

|

|

The Cost of Late Adoption

By Mark Coxon

rAVe Blogger

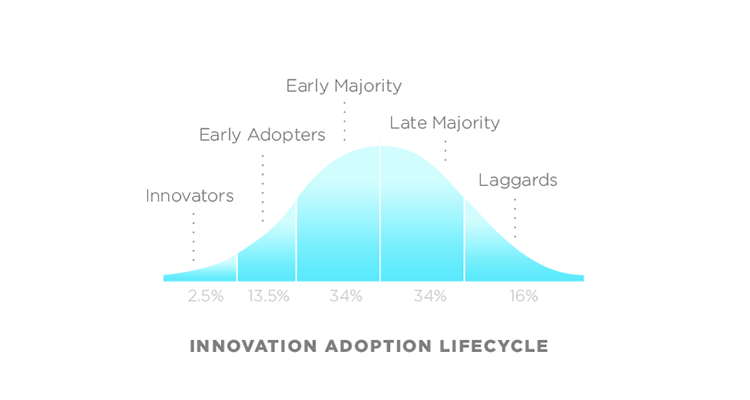

If you are a student of technology adoption, you’ve most likely seen this curve.

It’s the Technology Adoption curve and it reveals how people adopt technology over time. Looking at the curve as an integrator, you may use this curve to justify a delayed entry into a tech market. After all, around 70 percent of consumers don’t come into the market until the middle. If you take that viewpoint, you’re not alone. In fact, according to data I heard come out of the InfoComm standards plenary, integrators seem to adopt new technology into their businesses in almost exactly the same way consumers do, with the majority waiting for the swell in the middle. I think that this is a major mistake.

Before you start to disagree too much, let me lay out why I think there is a unique advantage for integration companies to be innovators and early adopters when it comes to offering new products and services in their businesses.

First off, it’s a marketing and sales advantage. 70 percent to 85 percent of the integration community is probably not telling this new technology story to their clients yet. That’s a great advantage when pitching a job, especially if the client is tech conscious or savvy themselves. However, I think there is a unique advantage in the actual numbers as well.

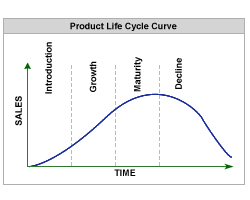

Let’s look at another common curve. The Product Life Cycle curve.

This curve, when over laid on the Technology Adoption curve above, shows that most integrators are waiting until growth has been demonstrated or sometimes even until the product has reached full maturity. This may not sound like a bad thing. In fact, the terms growth and maturity seem to denote stability.

But stability and profitability are two different things.

Now given all of the above let’s look at a couple curves I came up with in thinking through this adoption trend.

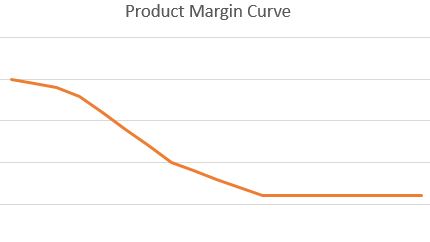

The first is the product margin curve.

When a product is first introduced and is novel or innovative, higher prices will be paid by consumers. Given this, typically products have higher margins as they are introduced and as the product reaches maturity and then market saturation, those margins fall and then level off at some small differential above the manufacturing costs.

But selling the product is only half of your integration business. Unless you are a box mover, you are selling installation, programming and support services with these products as well — so you also have a Labor Margin curve to factor in here as well.

Notice anything? It’s almost the opposite of the Product Margin curve. In the beginning, when a technology is new, your integration firm will inevitably spend more time training and installing the product, troubleshooting errors, etc. However, as the product reaches maturity, labor margins increase with the efficiency of the installations, programming and support of the product.

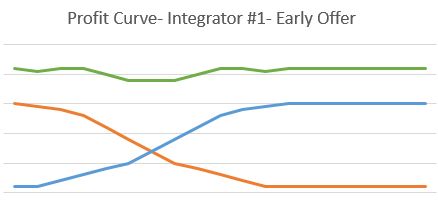

Given this, you really need to look at the sum of both graphs to get a good picture of the Profit curve of a integrating a new technology. If the product costs and integration costs are about equal, then you get something like this.

As you can see the green line is the sum of the two margin curves for Product (orange) and Labor (blue). Of course depending on the price of the product(s) in the system, these curves could move slightly. The point is however that in the example above, the integrator in question adopts the technology early. This means that the product margins offset additional labor expenditure during the learning phase, and then as product margins decrease, the integrators experience with the product provides advantages in actual integration costs to increase labor margins. Overall, the two competing curves can level each other out, creating a stable profit line over time for the technology itself.

But what happens to the integrator who waits?

A delayed entry into the market in growth or maturity mode means that the integrator will not take advantage of early, higher product margins. However, the labor margin curve remains. As an integrator, it still takes your team some time to become familiar with the technology and gain those economies. The result is a product margin curve that remains the same and a labor margin curve that is delayed.

As you can see the delayed entry affects the stability of the green profit line. If you look at the curve profit curve above, you’ll notice that profit actually decreases initially, and that many times causes an integrator to rethink their entry into the new market and perhaps retreat, not knowing that the trend is a direct result of the late entry, and will at some point climb back up as efficiencies in installation and programming are realized.

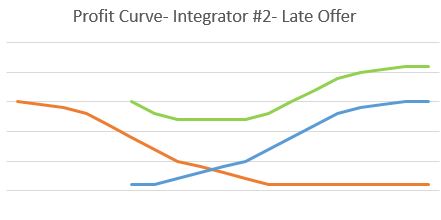

If you want to compare the profit curves of integrator 1 and integrator 2, it looks something like this.

If you take a look at the two profit curves above, an early entry into the market not only allows Integrator 1 (dark green) the opportunity to turn profit for more time than Integrator 2 (light green), but also gives them an advantage in profit during a huge portion of the Technology Adoption cycle as a whole. They have earned higher profits that allow them to be more competitive in a bid situation as well as present a longer track record of success with the technology.

All in all, the early adopter from an integration perspective can benefit greatly from adopting technology early, capturing a large percentage of early adopters and also creating advantages downstream as the technology matures that allows the same firm to continue an advantage until the product fades toward decline.

From a product manufacturing perspective, many argue that being second may be better than being first in that the follower can learn from the leaders mistakes. That may also be true here with integration if the delay to market is relatively small. However, even in manufacturing, no one argues that there is an advantage to entering the market in the middle or at the end. It may be a good time to look at the way your integration firm is adopting new technology to see if you’re benefiting from an early mover advantage.

I’d love to hear your take here. Feel free to use the comments below to start the conversation. Leave a Comment

Share Article

Back to Top |

|

|

Lean Model to Determine Designs

By Scott Tiner

rAVe Columnist

We have all heard, “Well that is how it was designed.” Or, “the integrators made this more complicated than it needed to be.” I, as much as anyone like to pass the buck, but when dealing with customers we need to make sure we provide the end result they want. A lean model of looking at design can help integrators provide the desired result the first time around, improving their relationships, reputation and future revenue stream.

The first step is to look at the Current (as designed) State. This is the state of how something operates right now. So, if you were looking into installing digital signs in a location that previously had corkboards, you would want to know several things about the current state.

- Are there rules about what gets posted on the bulletin board?

- How often is the bulletin board cleared off?

- Who “owns” the bulletin board?

The next step, and maybe the most critical, is to determine the Current (as-is) State. This is the way that things actually work. So, that list of rules you were given about what gets posted on the current bulletin board, does anyone actually know them, or follow them? If they tell you the bulletin board is cleared off on a weekly basis, does that actually happen?

Why are these types of questions important? Because if you design a system according to the as designed state, but that is not the actual as-is state, you are going to have unhappy customers. In the bulletin board example, if there are a bunch of rules, you will build the ability to follow these rules into a new digital signage system. This may cost development time, or a higher cost for the software. However, what if the customer never actually follows any of those rules? You have provided them what they asked for, but not for what they wanted. You have given them a product that costs more than what they need, and possibly added complexity to the system. Additionally, the person who suddenly has to monitor all those rules will feel as though this has caused them more work. Alternately, what if the people tell you they never follow the rules, but that they really want to start? This is critical to know before you design the system as well. Otherwise, you may observe them not following the rules, and build a system that does not allow them to enforce the policies they want.

So they key for these first two steps is to first determine how the current process/system is supposed to work. Often, that will not be how it actually works. Second, you need to determine how the system does actually work.

Now you have what you need to determine the Future (to-be) state. This is where you determine what the design of the new process/system will be. You need to put together what you have learned from the first two steps. As you work through this final step you should reference all the other things you have learned, and observed, through the first two steps. Now, you can start your design. When you present the final design to the customer, you should include your observations of all three states. Make sure you give them the opportunity to correct any of the observations or facts that you have collected. It is only through these steps that you and the customer can be on the same page about what they want. When that happens, you won’t hear the types of things that I wrote in the first sentence. Rather you will hear customers who are very happy with what you provided them. This means they will call you next time they need an upgrade or service. Leave a Comment

Share Article

Back to Top |

Click above to learn more

|

|

|

A Crack in the Wall Between the Real and Virtual Worlds

By Leonard Suskin

Pixel and Ink-Stained Wretch

Assuming that you’ve not been living under a rock, you’ve at least heard about the Pokémon GO! craze. For the uninitiated, Pokémon Go is an augmented reality game produced by Niantic (in partnership with Nintendo, which owns the rights to the intellectual property on which it is based) in which one needs to hunt the titular Pokémon in the real world. Pokémon, once captured, can be trained, leveled up, and used to battle for control of Pokémon gyms, which are also real-world locations. It is, at the very least, an excuse for gamers to get out and have some exercise. For those of us in the AV industry, it brings the idea of augmented reality to the forefront in a way it hasn’t been before — even by similar AR games. So what does it mean to us? Perhaps nothing. Perhaps everything. More likely something in between.

What Is It?

This is not Niantic’s first game. In fact, Pokémon Go! Is based on the game engine originally developed for the science-fiction AR game Ingress in 2012, when Niantic was still part of Google. Those who’ve played Ingress recognize familiar elements. Important real-world locations (post offices, public art, libraries, etc.) become in-game locations — “gyms” over which you battle against opposing Pokémon and “Pokéstops” at which one can replenish in-game supplies. As with Ingress, the game is entirely dependent on your phone’s GPS and data connection.

Each game is built around a secret-history fantasy narrative in which the game world is presented as an aspect of the real world which is hidden from most ordinary people. For Pokémon players it is the existence of magical beasts; for Ingress it is the incursion of extradimensional entities called “shapers” into our world. In neither case is the story all that important; it takes a back seat to gameplay.

The new gameplay element in Pokémon Go is a visual augmented reality element to add to the location-based augmented reality. The first augmentation to our reality — that the water tower is really a Pokéstop in which one can replenish supplies — is familiar to Ingress players. The second comes when one faces an actual Pokémon and can see the creature on ones phone screen, superimposed on the real-world image from your camera. In some environments, the game engine appears smart enough to set the Pokémon on the ground or other solid surface; in others it seems to randomly float about, not terribly well integrated at all with its environment. While the cartoonish-looking Pokémon lacking the detail or realism for their appearance to be truly immersive, their visual presence in the real world is another step towards connecting game world with real world. Seeing a Pokéball bounce on the sidewalk at someone’s feet is a striking experience and represents a crack in the wall between the real and virtual worlds.

Monetization?

It can also be used to drive behavior. AV blogger and podcaster Corey Moss (@cbmoss, July 15, 2016) noted the following on Twitter: “I saw how an AV integrator has become a #Pokestop – is this the new way to find customers? #AVTweeps”

I don’t know how much the average AV integrator relies on walk-bys (I’d guess somewhere between “none” and “absolutely none”), but Moss does have a point. Remember I said that post offices, libraries and other noteworthy public buildings are Ingress portals? I missed a category: Every Duane-Reade store is also a portal. I am certain this was a deal with Duane-Reade to increase foot-traffic to their stores. Of course, foot traffic does more for a pharmacy/convenience store than it will for an AV integrator — though I can see an intriguing idea in sending people to an AV contractor’s more striking public projects if one could also call attention to them and highlight who it was that installed them.

The interesting thing here is that you have dual potential avenues to make money — one more insidious than the next. Think about this: It is possible, given the correct digital incentives, to influence where people go in the real world. It isn’t mass mind-control, but it’s something similar.

The Bigger Picture?

The question AV professionals are now asking each other is whether or not there is a bigger picture — if the broad adoption of this toy is a sign that AR or VR might be moving close enough to mainstream adoption to have an effect on what we do. I’ll say yes and no; yes in that AR and VR are each becoming prevalent enough and low enough cost that we need at least ask the question. The story twenty years ago was of advanced technology from the boardroom making its way to the living room. Over the past decade, the new story has been residential technology filtering up towards the corporate world. We now may be moving past residential and towards personal mobile technology. For thirty dollars you can put a cardboard box around your phone and turn it into a VR headet. For free you can download toys like Ingress or Pokémon Go.

Gary Kayye came closest to explaining the paradigm shift in saying that we each hold a “personal information device” which, in some ways, replaces a large-scale display. Another way of framing it is that a video display, a camera, a microphone and a loudspeaker are dispatched to everyone’s physical location at nearly any time.

One can send content to a display and a loudspeaker in nearly any location. And receive content from a camera and a microphone (and other sensors).

We talk often about unified communication, and unified communication strategies. VR and AR may not be complete solutions, but they can become part of a unified content distribution strategy.

Again — What Is It?

To understand the viral phenomenon of Pokémon Go and its sudden reach is a study in marketing and public relations. That’s important, but not everything; what’s important to us is to see what this tells us about technology, what has actually been built and what that means. Can something else be built upon it? Is it proof of concept to build something different entirely? Is it a metaphor?

So what is Pokémon Go? It is:

- The Game Engine. A software tool which first formed the basis if Ingress and is now being turned to a different genre. The system for taking location and identity and turning it into interaction with objected overlaid onto the real world.

- Hardware. It is facilitated by ubiquitous hardware. You have a camera. You have a microphone. You have a display, you have a loudspeaker. And sensors to know where they are. Always.

- Infrastructure. GPS Satellites and wireless data, available in broad areas of the country. To make it work.

- Culture. A growing willingness to view part of life through our devices, a lack of inhibition about sharing our data — now including physical location in the real world.

Finally, Pokémon Go is the story Niantic and Nintendo built atop the software and hardware, facilitated by the existence of culture.

The hardware is there for everyone, as is the infrastructure and a new culture. It’s now up to us to find ways to use it. Leave a Comment

Share Article

Back to Top |

|

|

The Right Tool For the Job

By Hope Roth

They say that a poor craftsman blames their tools, but anyone who has ever tried to crimp a cable with a dull punch-down tool knows that you can only do so much with what you are given. It won’t fit on a coffee mug, but a less pithy way of putting it is “a fine craftsman knows the limitations of their tools and plans accordingly.”

What does that mean? It means knowing what you’re going to need onsite and planning accordingly. It also means keeping your work bag and vehicle stocked with things that you *might* need. It means keeping your equipment in good working order. In my case, it also means making sure that you have snack on hand (more on that later).

First things first, my work bag. I go to job sites using planes, trains, and automobiles, so all of the essentials have to fit in one bag. I also want to be able to walk without pain, so I can’t overload myself too much. This is what I carry:

- My laptop and power supply. That power supply is mission critical, so I have a spare that I use in my home office. That way, I never forget to grab it when I’m on my way out the door.

- A big-ass iPad. I use this as a mobile hot-spot, for filling out job paperwork, and as a second monitor when I’m stuck writing code while sitting on an over-turned paint bucket. I use a $10 app called Duet that lets me extend my screen onto my iPad. It was the best $10 I ever spent (big-ass iPad not included)

- Phone charging cable, charging brick, and a little batter pack that doubles as small Wi-Fi router. Nothing kills a phone battery like keeping it inside an electrical closet. I need to be able to charge my phone six ways from Sunday. I like gear that can pull double duty, so I got a battery pack that I can use for some temporary Wi-Fi if I need it.

- Extra-long USB cable and about eleventy-billion adapter cables for it. All of the different USB cables I needed were weighing me down, so I got one long one and then bought a box of adapters for it.

- Assorted proprietary cables, remotes, etc. This is all going to vary depending on what your job duties are.

- I’m a programmer, so I have the joy of carrying around an RS232 to USB adapter. I also do a lot of commercial lighting, so I carry Crestron remotes for setting up occupancy sensors and power packs.

- An extra-long Ethernet cable, as well as a coupler for attaching it to another cable.

Tweaker, multi-tool (if the TSA hasn’t found it and taken it away from me), lipstick (I am a girl, after all).

The goal in loading up my bag is to never get to a job site and say “oh shit, I can’t do anything else until I find [random cable]. Everything that goes into my bag lives there, unless I’m getting on a plane and it’s pointy.

In my car, I keep a box of spare equipment (mostly older remotes, proprietary batteries, and occasionally a spare processor). I also have all the PPE I might need if I have to work on a construction site (hard hat, high viz vest, boots, safety glasses). I also keep a spare company polo in case of wardrobe malfunctions or last-minute service calls.

My car is also where I keep all of the bigger/sharper/heavier tools that I’m not likely to need on a basic job, but which might come in handy in a pinch. This is where I store my multi-meter, punch-down tools, wire-strippers, etc.

And, most importantly, I have a box with snacks, non-perishable lunch packs and juice boxes. The juice boxes are technically for my young daughter, but they have worked in a pinch when I stuck in the middle of nowhere and getting increasingly thirsty/hungry and needed that little bit of sugar water.

Why do I consider snacks to be an essential job tool? Well, you wouldn’t like me if I’m hangry. My job often takes me to places where lunch isn’t readily available. I need to be able to keep my blood sugar at a decent level, or I’m never going to get any work done.

Everything in my car (theoretically) lives in a couple of crates that can be pulled out and stored if we’re going on a family trip and I need the cargo space. Although, if you ask my husband, it tends to take over the entire trunk of my car.

So, there you have it, my essential tools list. Is there anything you think I’ve missed? What’s in your tool bag? Leave a Comment

Share Article

Back to Top |

|

| Global Sales of Solid State Projectors Soar 17 Percent Year-on-Year in CY Q2 2016 Futuresource Consulting has revealed its latest insights into the worldwide projector market which highlight that the market has declined 4.6 percent year-on-year in CY Q2 2016 to 1.76 million units, with value falling 5.6 percent to $2 billion. Despite value falling further than volume for another consecutive quarter, the disparity is far weaker than previously seen, a positive sign that average selling prices (ASPs) are in recovery.

Senior Market Analyst Claire Kerrison commented, “Whilst the market witnessed further declines this quarter, this was largely driven by macro-economic or political factors in key emerging regions, rather than just the impact of competing display technologies. The fact that the rate of market value decline has diminished is incredibly encouraging. Value was propelled by sales of solid state solutions, increasing 17% during the quarter, which now attributes to 8% of total sales.”

Futuresource expects that as solid state adoption continues to mount it will drive an increase in ASPs and consequently a rise in overall market value, despite a decrease in volume.

Kerrison added, “There are positive stories among the overall market declines. Sales of 1080p and WUXGA enjoyed a combined growth of 38 percent year-on-year. Furthermore, sales of 5-7K lumen products continue to rise, with sales up 22 percent year-on-year. It should not be forgotten that there are opportunities for projector brands out there.”

All the details are here. Leave a Comment

Share Article

Back to Top |

|

| AMETEK Electronic Systems Protection Adds Predictive Maintenance Technology to ESP/SurgeX BrandsSurgeX appears to be blowing away their competition with intelligent surge products. And, I don’t say this lightly as there are some big-brands and names in this business. But, AMTEK buying them was a major coup. AMETEK Electronic has added their intelligent diagnostics, and remote monitoring solution to almost the entire ESP/SurgeX line. Branded as Expert Manager, it provides analysis of a complex array of power-related data with the ability to translate that data instantly into reports that pinpoint problems and offer solutions to solve them.

Expert Manager is the first software tool in the industry that analyzes a wide range of conditions and issues, such as electrical parameter data, under-voltages, over-voltages, or power outages and surges. It provides various solutions to mitigate problems at the touch of a button. When combined with ESP/SurgeX cloud capabilities, Expert Manager also can send power quality alerts to users as a preventative measure.

An integrated analytics tool offers a corrective course that can be as simple as adjusting an abnormal load, or something more serious like contacting an electrician to correct excessive neutral-ground voltage. Expert Manager is designed to help keep connected equipment running smoother without disruption, against a wide variety of power issues.

Here are the tech specs. Leave a Comment

Share Article

Back to Top |

| Legrand Ships HDMI Cables Supporting 4K, HDRLegrand is introducing Premium High Speed HDMI cables with Ethernet, the company’s first that offer full support of 4K and High Dynamic Range (HDR).

Legrand’s eight-piece offering includes two white slim line cables, the AC3MP1-WH (one-meter length) and AC3MP2-WH (two-meter length), which are ideal for discreet installations, such as wall-mounted monitors, as they maintain the lowest profiles without sacrificing features or performance. Rounding out the group are an array of black cables that range in size from one to seven meters — the AC2MP1-BK, AC2MP2-BK, AC2MP3-BK, AC2MP4-BK, AC2AP5-BK and AC2AP7-BK.

All the cables are certified to handle 18 Gbps data speeds and the packaging for each cable features a QR code and a unique holographic fingerprint that consumers can scan with their mobile devices to verify that the manufacturer and model number are authentic and certified as they are making their purchasing decisions.

All of Legrand’s Premium High Speed HDMI cables are constructed of PVC molding housing, gold-plated and CL-3 rated for in-wall use. They have small overmold designs that allow them to be pulled more easily between studs during installation. To facilitate the use of these cables in more applications, Legrand also offers the HT2102-WH-V1 flat panel TV connection kit.

Here are the details. Leave a Comment

Share Article

Back to Top |

| AudioControl Launches Architect ‘P’ Series Amplifiers AudioControl is finally shipping their Architect series of multi-channel amplifiers in 12 or 16 channel options. The Architect ‘P’ Series delivers over 100 watts per channel into 8 ohms, 200 watts per channel into 4 ohms, all channels driven. Additional adjoining channels can be bridged to 400 watts. The Architect ‘P’ Series uses a cool running proprietary design, including AudioControl’s LightDrive anti-clipping protection, input bussing capability, output pass-thru, master 12v trigger in/out plus local 12v trigger inputs on all zones, signal sensing as well plus digital inputs through a SPDIF input for digital sources.

The Architect ‘P’ series is available in a robust anodized black finish and is designed, engineered and manufactured at AudioControl’s manufacturing facilities located in Seattle, USA! AudioControl has announced four new Architect ‘P’ Series models. These models are the Architect Model P2680 EQ (16 Channels, 100w, Equalization), the Architect Model P2660 (16 Channels, 100w), the Architect Model P2280 EQ (12 Channels, 100w, Equalization) and the Architect Model P2260 (16 Channels, 100w).

Here are the details. Leave a Comment

Share Article

Back to Top |

|

| PureLink Debuts Locking Screw HDMI Cables PureLink today announced the availability of its new line of “locking” HDMI cables, under its TotalWire brand. The cables support HDMI 2.0b technology as well as the transmission of HDR (High Dynamic Range) content and have a screw-based locking feature that prevents strain and loose connections and could eliminate the need for additional port savers or brackets.

The PLH Locking Screw HDMI cables are spec’d at 18Gbps of bandwidth for use with HDMI v.2.0b. They also offer HDR, CEC and HDCP 2.2 compliance to support multi-dimensional immersive audio content and dynamic control options. The PLH has multi-layer shielding, for EMI protection, and supports 4K@50/60 (2160p) at 4:4:4 color format. The new locking screw cables come in a variety of lengths, including 1, 2, 3 and 5 meter (3.3, 6.6, 10 and 16.5 feet) cables.

Here they are. Leave a Comment

Share Article

Back to Top |

| Atlona Ships Eight-Output 4K/UHD Distribution Amplifier Atlona announced it is now shipping its eight-output 4K/UHD distribution amplifier that features HDMI-to-HDBaseT distribution of 4K/UHD @ 60 Hz (4:2:0 Chroma sampling) video, HDBaseT transmission up to 70 meters, HDCP 2.2 support, and Power over Ethernet (PoE). The AT-UHD-CAT-8 also provides EDID management and advanced display control functions through Consumer Electronics Control (CEC) for use with home TVs.

In addition to HDBaseT outputs, the new DA provides an HDMI output for signal pass-through and daisy-chaining, and it is equipped with one IR and RS-232 connection for the amp as well as one for each output channel.

The AT-UHD-CAT-8, which is rack-mountable and fits in one full-width single RU space, lists for $2,299 and it’s here. Leave a Comment

Share Article

Back to Top |

|

| James Loudspeaker Adds a High-Output Small Aperture Architectural Speaker James Loudspeaker has added to their lineup of Small Aperture (SA) architectural speakers with the introduction of the 63SA-7HO high-output in-ceiling loudspeaker. The 63SA-7HO is a three-way speaker system featuring greater sensitivity than prior models and a new 6.5-inch woofer capable of higher output.

The James Loudspeaker 63SA-7HO features what hey claim is “aircraft-grade” aluminum construction and a modular design, providing long life and easy service, while the built-in limiter offers the utmost in long term reliability. The 63SA-7HO’s compact footprint and 7-inch depth is best suited for in-ceiling applications. The SA series of speakers is available with an array of 3-inch round and square grilles and has also been designed to accept industry standard 3-inch and 4-inch lighting trim kits to allow seamless integration with similarly styled lighting products.

The James Loudspeaker 63SA-7HO utilizes proprietary drivers including a 6.5-inch aluminum woofer, a 2-inch midrange and a ¾-inch tweeter.

The 63SA-7HO is $1,400 and here are the details. Leave a Comment

Share Article

Back to Top |

|

For all you REGULAR readers of rAVe HomeAV Edition out there, hopefully you enjoyed another opinion-packed issue!

For those of you NEW to rAVe, you just read how we are — we are 100% opinionated. We not only report the news and new product stories of the high-end HomeAV industry, but we stuff the articles full of our opinions. That may include (but is not limited to) whether or not the product is even worth looking at, challenging the manufacturers on their specifications, calling a marketing-spec bluff and suggesting ways integrators market their products better. But, one thing is for sure, we are NOT a trade publication that gets paid for running editorial or product stories. Traditional trade publications get paid to run product stories — that’s why you see what you see in most of the pubs out there. We are different: we run what we want to run and NO ONE is going to pay us to write anything good (or bad).

Don’t like us, then go away — unsubscribe! Just use the link below.

To send me feedback, don’t reply to this newsletter – instead, write directly to me at gary@ravepubs.com or for editorial ideas: Editor-in-Chief Sara Abrons at sara@ravepubs.com

A little about me: I graduated from Journalism School at the University of North Carolina at Chapel Hill (where I am adjunct faculty). I’ve been in the AV-industry since 1987 where I started with Extron and eventually moved to AMX. So, I guess I am an industry veteran (although I don’t think I am that old). I have been an opinionated columnist for a number of industry publications and in the late 1990s I started the widely read KNews eNewsletter (the first in the AV market) and also created the model for and was co-founder of AV Avenue – which is now known as InfoComm IQ. rAVe Publications has been around since 2003, when we launched our original newsletter, rAVe ProAV Edition.

rAVe HomeAV Edition, co-published with CEDIA, launched in February, 2004.

To read more about my background, our team, and what we do, go to https://www.ravepubs.com Back to Top |

Copyright 2016 – rAVe [Publications] – All rights reserved. For reprint policies, contact rAVe [Publications], 210 Old Barn Ln. – Chapel Hill, NC 27517 – 919/969-7501. Email: sara@ravepubs.com

rAVe HomeAV Edition contains the opinions of the author only and does not necessarily reflect the opinions of other persons or companies or its sponsors. |

|

|

|