LCD TV Brands’ Production Expected To Reach Record High in October

By David Hsieh

DisplaySearch

Since Q2’14, LCD TV panels have been in tight supply due to increases in purchasing by some leading LCD TV brands. As shown in our Monthly Large-Area LCD Pricing Report, prices for mainstream sizes (32”, 40”, 42”, 48”/49” and even 50”, 55”) have been increasing. In Q3’14, we reported that leading TV brands Samsung and LG Electronics increased their 2014 annual business plan to 48M and 34M units, respectively, which has helped the LCD TV panel — especially open cell — shortage to continue. Chinese TV makers also are gearing up for the Q4’14 and 2015 holidays, and are increasing their panel forecasts.

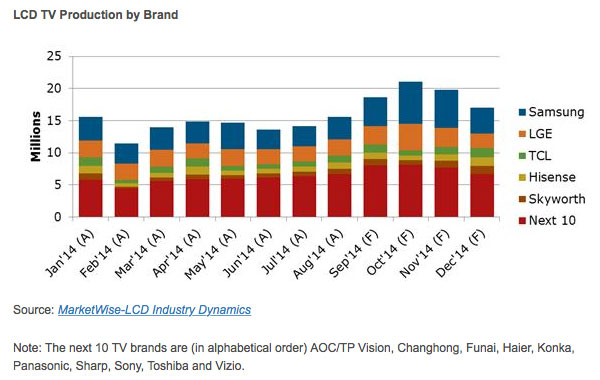

As reported in MarketWise-LCD Industry Dynamics, the top 15 LCD TV brands produced 15.5M LCD TVs in August, the highest monthly total since January. Preliminary estimates are for the production amount to reach 18.7M in September, which would be 9 percent growth Y/Y.

As TV brands continue to increase production in response to strong market pull and in preparation for the holiday seasons, we expect the top 15’s production will reach 21.1M in October, which will be 15 percent growth Y/Y, which as we show would be not only the highest this year, but ever. We then expect monthly production to fall, but maintain a higher level than in Q3.

October is typically the seasonal peak for global TV production and set shipments, but the record high expected this year shows how determined the TV brands are to see strong Q4 sales. In fact, many leading brands, including Samsung, LGE, Sony and Chinese, have reduced retail prices (for some models by double digits) in an attempt to stimulate sell-through.

All of the top 15 brands are expected to increase October production except Chinese TV makers, who are facing fewer working days due to the October National Holidays. But brands like Samsung and LGE in particular are increasing October production and shipment plans by more than 40 percent M/M. Samsung and LGE accounted for 48 percent of global revenues in Q2’14, according to the Quarterly Global TV Shipment and Forecast Report, so they have great power over panel allocation and price negotiation.

For panel makers, the strong uptick in October and the still-strong TV production in Q4’14 could indicate that panel demand will not fall drastically and will remain in tight supply in Q4. While excess panel shipments in Q2 caused concern for panel inventories, TV makers’ strong production plans may indicate that inventory might not be much of a concern, at least for the rest of this year.

More Stories Like This

NSCA Releases 2022 Compensation & Benefits Report

NSCA has just released its 2022 Compensation & Benefits Report, which is based on data gathered from systems integrators across North America. Now in its seventh iteration, the report tracks and benchmarks compensation and benefits data for a variety of key positions within the industry, including technical, non-technical and C-suite roles. Systems integration firms of all sizes and […]

Frost & Sullivan’s Global Video Conferencing Report: Global UCC Devices to Be Up 6x by 2025, With Revenues of $7.8 Billion

As businesses and educational institutions prepare for the return to work, meeting rooms and classrooms will see heavy technology investments to support hybrid work and learning. Frost & Sullivan’s recent analysis, State of the Global Video Conferencing Devices Market, Forecast to 2025, finds that by 2025, the number of video conferencing devices, including room-based endpoints, […]

How Will Installation Verticals Weather the Storm of COVID-19?

By James Kirby Futuresource Consulting Through its research in recent years, Futuresource has identified the install audio markets as a key opportunity for brands across the professional audio industry, ranging from large system touring vendors, through to business music brands and conferencing microphone suppliers. However, as with many professional audio segments and other areas of […]